Beginner's Roadmap to Financial Wealth: A Step-by-Step Guide to Building Long-Term Wealth

Financial wealth isn’t something that just happens—it’s built through intentional planning, disciplined habits, and a clear roadmap. Whether you're just starting out or looking to get back on track, understanding the steps to build long-term wealth is essential. This beginner's roadmap to financial wealth will guide you through the key principles and strategies to help you take control of your money and work toward a more secure, prosperous future.

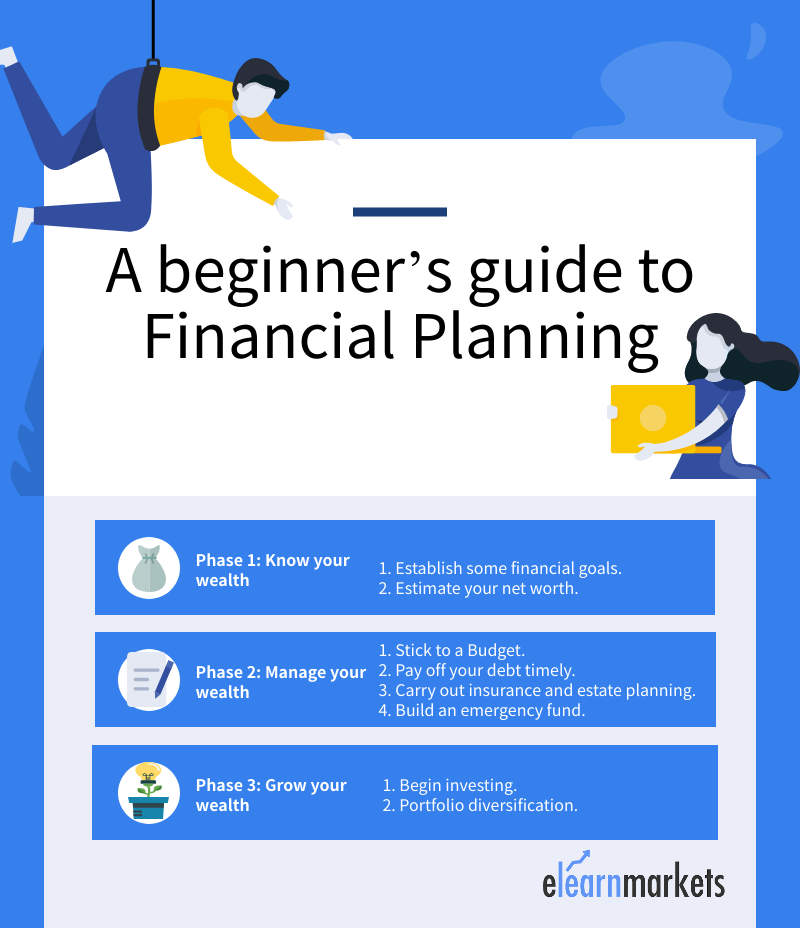

Understanding Your Current Financial Situation

The first step in building wealth is to understand where you are financially. This means taking stock of your income, expenses, debts, and savings. Start by listing all your income sources—salary, side hustles, investments, etc.—and then track your monthly expenses. Use tools like budgeting apps or spreadsheets to categorize your spending into essentials (rent, groceries, utilities), debt payments, and discretionary spending (entertainment, dining out).

It’s also important to check your credit report and score. This gives you insight into your borrowing power and helps identify any errors or hidden debts. Knowing your financial standing allows you to create a realistic plan that reflects your current situation.

Setting Clear Financial Goals

Once you have a clear picture of your finances, it’s time to set goals. These should be specific, measurable, and time-bound. For example, instead of saying “I want to save money,” aim for something like “I want to save $5,000 for an emergency fund within six months.”

Prioritize your goals based on urgency and importance. Short-term goals might include paying off high-interest debt, while long-term goals could involve saving for retirement or buying a home. Writing down your goals and revisiting them regularly keeps you motivated and on track.

Creating a Realistic Budget

A budget is the foundation of financial stability. It helps you allocate your income wisely and avoid overspending. There are several budgeting methods to choose from, such as the 50/30/20 rule, which divides your income into 50% for needs, 30% for wants, and 20% for savings and debt repayment. Alternatively, zero-based budgeting assigns every dollar a purpose, giving you full control over your spending.

The key is to find a method that works for you and stick to it. Consistency is more important than perfection. Even small adjustments can lead to significant improvements over time.

Building an Emergency Fund

Life is unpredictable, and unexpected expenses can derail even the best-laid plans. An emergency fund acts as a financial safety net, helping you cover unforeseen costs without resorting to high-interest debt. Aim to save three to six months of living expenses in an accessible account, such as a high-yield savings account. If this target seems daunting, start with a smaller goal, like $500 or $1,000, and build up gradually.

Keep your emergency fund separate from your other accounts to avoid the temptation to spend it on non-emergencies. Replenish it as soon as possible if you need to use it, and remember that having this buffer provides peace of mind and financial security.

Saving and Investing for the Future

After establishing an emergency fund, focus on long-term savings and investments. Retirement accounts like 401(k)s and IRAs offer tax advantages and allow your money to grow through compound interest. Take full advantage of employer matching contributions whenever available, as this is essentially free money.

Beyond retirement, consider investing in a diversified portfolio of stocks, bonds, mutual funds, and index funds that align with your risk tolerance and financial timeline. Diversification reduces the impact of market fluctuations and increases the potential for growth over time. For those with a longer time horizon, real estate or entrepreneurial ventures can also be powerful wealth-building tools.

Reviewing and Adjusting Your Plan

Your financial plan shouldn’t be static. Life changes, and so should your approach to managing money. Schedule regular reviews of your finances—perhaps once a year—to assess your progress and make necessary adjustments. Tools like financial apps or spreadsheets can simplify this process, allowing you to track your spending, debt, and investments effectively.

Life events such as job changes, marriage, the birth of a child, or the loss of a loved one can significantly impact your financial situation. Be prepared to revisit your goals and adjust your strategies accordingly. Flexibility and adaptability are key to long-term financial success.

Common Mistakes to Avoid

Many people fall into common financial traps that hinder their progress. One of the most frequent mistakes is not having a budget. Without a clear plan, it’s easy to overspend and lose track of your money. Another mistake is underestimating the importance of an emergency fund. Many people save too little, leaving themselves vulnerable to unexpected expenses.

Neglecting retirement savings is another critical error. The earlier you start, the more time your money has to grow through compound interest. Additionally, failing to monitor and adjust your financial plan can lead to missed opportunities and stagnation. Stay proactive and committed to your goals.

Benefits of Working with a Financial Planner

While many people manage their finances on their own, working with a financial planner can provide valuable guidance and expertise. A financial advisor can help you create a personalized plan based on your unique circumstances, offering objective insights and ongoing support. They can also help you navigate complex situations, such as debt management, investment strategies, and estate planning.

If you’re unsure where to start, consider consulting a certified financial planner (CFP). They can help you develop a comprehensive strategy that aligns with your goals and values, providing the accountability and expertise needed to stay on track.

Final Thoughts

Building financial wealth is a journey that requires patience, discipline, and a clear roadmap. By understanding your current situation, setting realistic goals, creating a budget, building an emergency fund, and investing for the future, you can take control of your finances and work toward long-term stability. Remember, the path to financial freedom is unique for everyone, but with the right mindset and strategies, it’s achievable.

{kind=link}

Post a Comment for "Beginner's Roadmap to Financial Wealth: A Step-by-Step Guide to Building Long-Term Wealth"

Post a Comment